Autonomous Driving in 2025: State of the Industry and the Road Ahead

This report provides a comprehensive analysis of the autonomous driving industry as of 2025, covering the technological landscape, key industry players, real-world deployments, regulatory challenges, and market trends across both passenger vehicles and commercial trucks. It evaluates the current state of autonomy (Levels 1–5) with data-driven insights on leading companies like Waymo, Tesla, Baidu, and Aurora, while outlining the hurdles and opportunities shaping the path toward broader adoption.

Bryn Pilney

Head of Research

Introduction: A Turning Point for Self-Driving Vehicles

After a decade of bold predictions, 2025 finds autonomous driving at an inflection point.

We're going to end up with complete autonomy, and I think we will have complete autonomy in approximately two years.

Robotic taxis are now a reality – Waymo’s driverless cars provide over 250,000 paid rides per week in U.S. cities – yet full Level 5 autonomy remains elusive. Massive investments and years of R&D are yielding tangible progress, but the journey has been more arduous than early hype anticipated. This editorial examines where the industry stands today, balancing hard data with insights on what’s next.

Technological Landscape

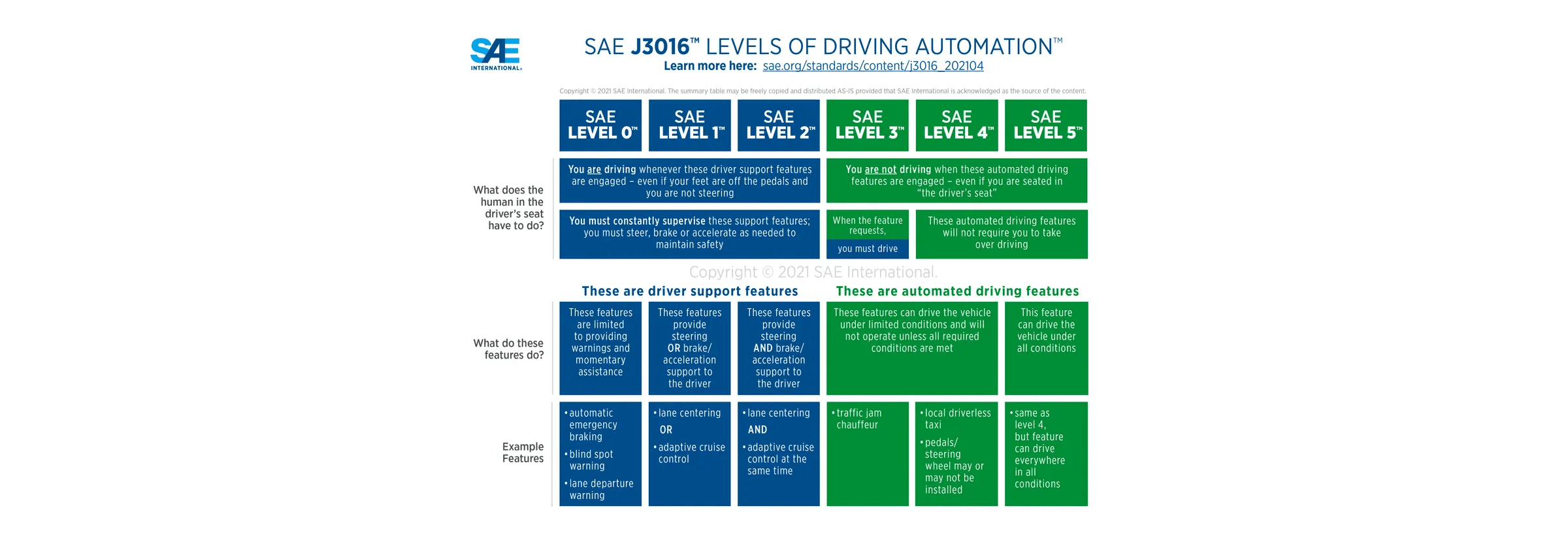

SAE Framework (L0-L5)

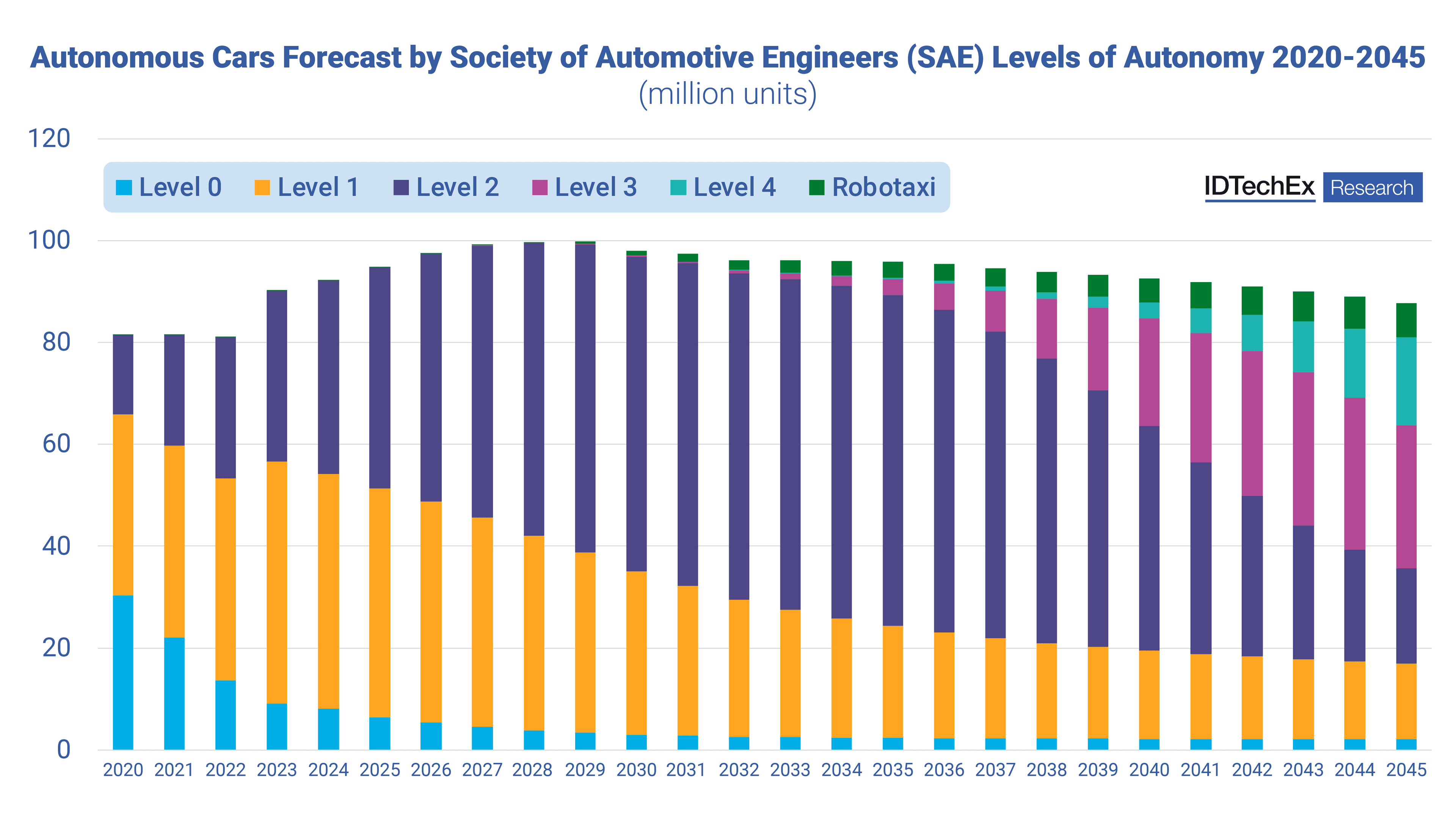

Autonomous driving is classified in six levels (0–5) defined by The Society of Automotive Engineers (SAE), from "No Driving Automation" (L0) to "Full Driving Automation" (L5).

Most personal cars today are Level 2 (partial automation with driver supervision), and a few systems have reached Level 3 (conditional automation in limited scenarios). True Level 4 robotaxis operate in geofenced areas, but no Level 5 vehicles (anywhere, anytime autonomy) are deployed yet in 2025.

Sensors and Compute

Modern autonomous vehicles (AVs) rely on a suite of complementary sensors— cameras for rich visual details, lidar for precise depth maps, and radar for robust detection in poor visibility—feeding a multilayered AI perception stack.

Different companies emphasize different sensor strategies: Waymo integrates cameras, lidar, and radar for detailed 3D mapping and robust multimodal sensing, while Tesla bets on vision-only perception using neural networks. Regardless of approach, all systems must ingest and process massive real-time data streams—with a single AV generating between 1.4 TB and 19 TB of sensor data per hour, depending on the number and type of onboard sensors.

AI in AV

Transformer models are a promising modern approach to sensor fusion, bringing greater accuracy but at the cost of higher computational demands and latency, pushing the limits of onboard processing. This enables the AV to “see” and react in milliseconds, solving a complex matrix of driving possibilities at every moment.

Thanks to progress in computer vision and reinforcement learning, autonomous systems have improved in handling scenarios like lane-keeping, adaptive cruise, and emergency braking.

However, the long-tail of driving (unusual situations, erratic human behavior, bad weather) remains a challenge. Ensuring reliability in these edge cases is an ongoing technical battle – requiring further breakthroughs in AI algorithms, sensor resolution, and perhaps new paradigms (from V2X communication to better simulation testing).

Real-World Deployments

Robotaxis

As of 2025, autonomous ride-hailing services (i.e. robotaxis) have transitioned from futuristic experiments into tangible realities in multiple cities worldwide.

Waymo

Waymo currently leads the market, operating fully driverless robotaxi services in Phoenix, San Francisco, Los Angeles, and Austin. By early 2025, Waymo’s fleet reached approximately 250,000 paid rides per week, accumulating millions of fully driverless rides—each trip building public confidence and demonstrating the viability of robotaxi operations. Expansions into Atlanta and Washington D.C. are planned for the coming years, signaling steady growth.

Apollo Go

In China, Baidu’s Apollo Go service has rapidly expanded, providing over 9 million cumulative rides by early 2025, with 1.1 million rides completed in Q4 2024 alone—a 36% year-over-year increase. Apollo Go now offers fully driverless rides (without safety drivers) across more than ten major cities, including Beijing, Shanghai, Wuhan, and Guangzhou. Baidu’s rapid growth was facilitated significantly by supportive government policies that designate specific urban zones for autonomous testing and commercial deployment.

Motional

Motional, originally a joint venture between Hyundai and Aptiv, has recently undergone significant ownership restructuring, with Hyundai increasing its stake as Aptiv substantially reduced its investment. Hyundai has committed nearly $1 billion in recent funding rounds, underscoring its belief in the strategic value of Motional’s technology despite Aptiv scaling back due to mounting financial losses. Motional has completed over 100,000 autonomous passenger rides in Las Vegas through partnerships with Lyft and Uber, and has conducted thousands of autonomous food deliveries in Los Angeles.

However, acknowledging the challenges of scaling autonomous ride-hailing in the near term, Motional is shifting its strategic focus away from immediate large-scale robotaxi deployments. Instead, the company now emphasizes the ongoing development and generalization of its Level 4 autonomous driving technology, positioning itself to capitalize on future opportunities when market conditions are clearer and technology maturity has advanced. This strategic pivot has led Motional to streamline its workforce, reflecting a broader industry trend towards a more measured and cautious deployment of autonomous vehicles.

Zoox

Amazon’s Zoox is taking a distinctly different path toward robotaxis, designing its own custom-built, electric, bidirectional vehicle that eliminates traditional elements like steering wheels and pedals. Zoox plans to scale production significantly in 2025, opening a larger facility in California’s Bay Area to transition from its current fleet of about two dozen test vehicles to potentially thousands of purpose-built robotaxis. The company aims to launch its first commercial ride-hailing services in Las Vegas later this year, with San Francisco to follow, marking a key step forward from internal testing and limited employee programs.

Despite its ambition, Zoox faces substantial hurdles. A recent crash involving an unoccupied Zoox vehicle in Las Vegas led to a temporary suspension of operations and a software recall affecting 270 vehicles, highlighting ongoing challenges in fine-tuning autonomous systems for real-world conditions. Still, Zoox remains confident in its unique approach, asserting that purpose-built robotaxis provide a superior passenger experience compared to retrofitted vehicles. While the path to broad adoption remains cautious, Zoox continues methodically refining its technology, positioning itself strategically within Amazon’s broader logistics and mobility ambitions.

Mobileye

In 2024, Mobileye advanced both its robotaxi ambitions and its industry partnerships. In June, European startup Verne (formerly Project 3 Mobility) unveiled a purpose-built autonomous ride-share vehicle powered by Mobileye Drive at the Rimac campus in Croatia. This six-passenger robotaxi is slated for urban service under the “Verne” mobility platform, showcasing Mobileye’s Level 4 technology in a real-world deployment. Mobileye also forged deals to scale its autonomous services: it teamed with Volkswagen’s ADMT division to deploy a fleet of self-driving vehicles – marking the first large-scale AV program by a global automaker. In the U.S., Mobileye entered an alliance with Lyft to make Mobileye Drive–equipped robotaxis available on Lyft’s network through fleet operators, tapping into Lyft’s 40 million riders to accelerate commercialization.

In the near future, Mobileye aims to launch driverless ride-hailing services in key markets pending regulatory approval. The company has signaled plans to phase out safety drivers in its robotaxi pilots, building on progress in Munich and Tel Aviv where Mobileye has vehicles ready for service once permitted. Its alliance with Lyft is expected to bear fruit in 2025, allowing riders in North America to hail “Lyft-ready” AVs outfitted with Mobileye Drive technology. Mobileye is also integrating its autonomous platform into consumer vehicles (for example, partnering with Zeekr and Polestar on eyes-off systems) as a bridge toward full autonomy. By mid-decade, through these collaborations and continuing tech improvements (such as incorporating lidar via partners like Innoviz), Mobileye plans to scale up robotaxi deployments across Europe, Israel, and the U.S., moving from pilot programs to broader commercial services.

Today, while robotaxis have proven technically feasible and commercially viable within clearly mapped and controlled areas, scaling these services beyond geofenced urban zones remains a critical challenge. Each successful deployment incrementally expands the boundaries of public acceptance, gradually reshaping urban mobility. Ultimately, the diverse approaches taken by these companies—from lidar-heavy mapping to camera-driven AI—demonstrate that the path to widespread robotaxi adoption will be competitive, collaborative, and continually evolving.

Autonomous Trucking

While robotaxis grab headlines, autonomous trucking is quietly transforming logistics.

Aurora

In May 2025, Aurora became the first company to commercially operate fully driverless trucks on public roads, launching autonomous freight runs between Dallas and Houston with no human onboard. These deliveries for Uber Freight and Hirschbach Motor Lines mark a significant milestone following years of rigorous supervised testing. Aurora’s Class 8 trucks have now logged over three million autonomous miles, completed over 10,000 pilot hauls, and the company plans to extend operations to routes connecting El Paso and Phoenix by the end of the year.

Kodiak Robotics

In 2024, Kodiak Robotics achieved major milestones in autonomous trucking, including the industry’s first fully driverless commercial deliveries in partnership with Atlas Energy Solutions. The company significantly expanded its long-haul operations, completing over 100,000 miles of autonomous freight with notable partners such as J.B. Hunt, Bridgestone, IKEA, Tyson, and Maersk. Kodiak also established a strategic truckport in Houston with Ryder, positioning itself for scaled deployment of fully driverless trucks across Texas and Oklahoma routes. These accomplishments underline Kodiak’s growing leadership role in bringing autonomous trucking closer to widespread commercial viability.

Gatik

Gatik continues to build momentum as a leader in autonomous middle-mile logistics, uniquely focusing on constrained routes connecting warehouses and retail stores. The company, which began fully driverless deliveries for Walmart in 2021, now operates autonomous fleets commercially across Texas, Arkansas, Arizona, and Ontario, handling frequent, repetitive short-haul logistics.

Recently, Gatik secured a strategic $30 million investment from Isuzu Motors, cementing a partnership aimed at mass-producing Level 4 autonomous trucks by 2027, complete with purpose-built redundant chassis designs optimized for safety.

To enhance its autonomous capabilities, Gatik also announced a collaboration with NVIDIA, integrating NVIDIA’s DRIVE AGX Thor computing platform to provide powerful onboard AI processing necessary for scalable commercial deployment.

These partnerships position Gatik to rapidly expand its fleet from over one hundred trucks in daily operation to thousands of autonomous trucks by 2027. As it grows, Gatik remains focused on solving critical industry challenges, including driver shortages, increasing delivery demand, and operational costs, offering Fortune 500 customers like Walmart, Kroger, and Tyson Foods safer and more efficient middle-mile logistics solutions.

Plus.ai

Plus (also known as Plus.ai) has focused on forging global partnerships and pilot programs to deploy its autonomous trucking technology at scale. In March 2024, Plus announced a landmark deal with Volkswagen’s TRATON Group – encompassing truck brands Scania, MAN, and Navistar – to co-develop Level 4 self-driving trucks using Plus’s SuperDrive autonomous system. Public road testing of these L4 trucks (with safety drivers) began in 2024 on freight corridors in both Texas and Sweden, and the partners plan to move into pilot freight operations with fleet customers by late 2024. This long-term alliance sets the stage for series production of autonomous trucks in the next few years, essentially embedding Plus’s driverless tech into future Scania and International models. Plus has also completed successful trials in Europe: in May 2025, it concluded a pilot in Germany with logistics firms DSV and dm-drogerie markt using an Iveco heavy truck outfitted with Plus’s system. That pilot saw an autonomous truck (with a human overseer) hauling goods between distribution centers, demonstrating improved safety and fuel efficiency in real-world conditions. These achievements come on top of Plus’s ongoing deployments of its driver-in “PlusDrive” highway automation in commercial fleets in China and the U.S., as well as tech collaborations with companies like Hyundai (pairing Plus’s software with hydrogen fuel-cell trucks for evaluation).

Plus’s forward-looking plans are centered on scaling from pilots to full commercial launches with its OEM and fleet partners. According to the TRATON partnership roadmap, 2024’s trials will be followed by series production of L4 trucks and global deployment “at scale,” targeting key freight routes in North America and Europe by 2025–2026. In Japan, Plus has entered a strategic partnership with open-source AV pioneer Tier IV as part of a government-supported initiative to deploy driverless trucks on expressways and alleviate the country’s truck driver shortage. That effort will integrate Plus’s AI “virtual driver” with Tier IV’s platform to create a custom solution for Japanese trucks, with testing slated to begin on closed tracks and highways in 2025. As these initiatives mature, Plus is positioning itself less as a standalone truck operator and more as an autonomy technology partner to the world’s leading truck manufacturers and logistics providers. The company is preparing its “Autonomy 2.0” software for production trucks and has hinted at a public listing in the near future to bolster its funding. If all goes to plan, the next couple of years will see Plus-enabled driverless trucks begin commercial runs on highways from Texas to Germany to Tokyo, underpinned by the robust alliances formed in 2024.

Together, these varied deployments illustrate how autonomous trucking has rapidly evolved beyond theoretical potential into practical solutions reshaping goods transportation. Unlike the complexities faced in urban autonomy, highway trucking offers a clearer path to immediate commercial viability due to its predictable environment and strong economic incentives. These emerging leaders suggest autonomy will reshape logistics from the ground up, beginning not with passengers, but with the everyday goods that sustain modern commerce.

Market Impact and Investment: Hype, Reality, and Opportunity

Investment Landscape

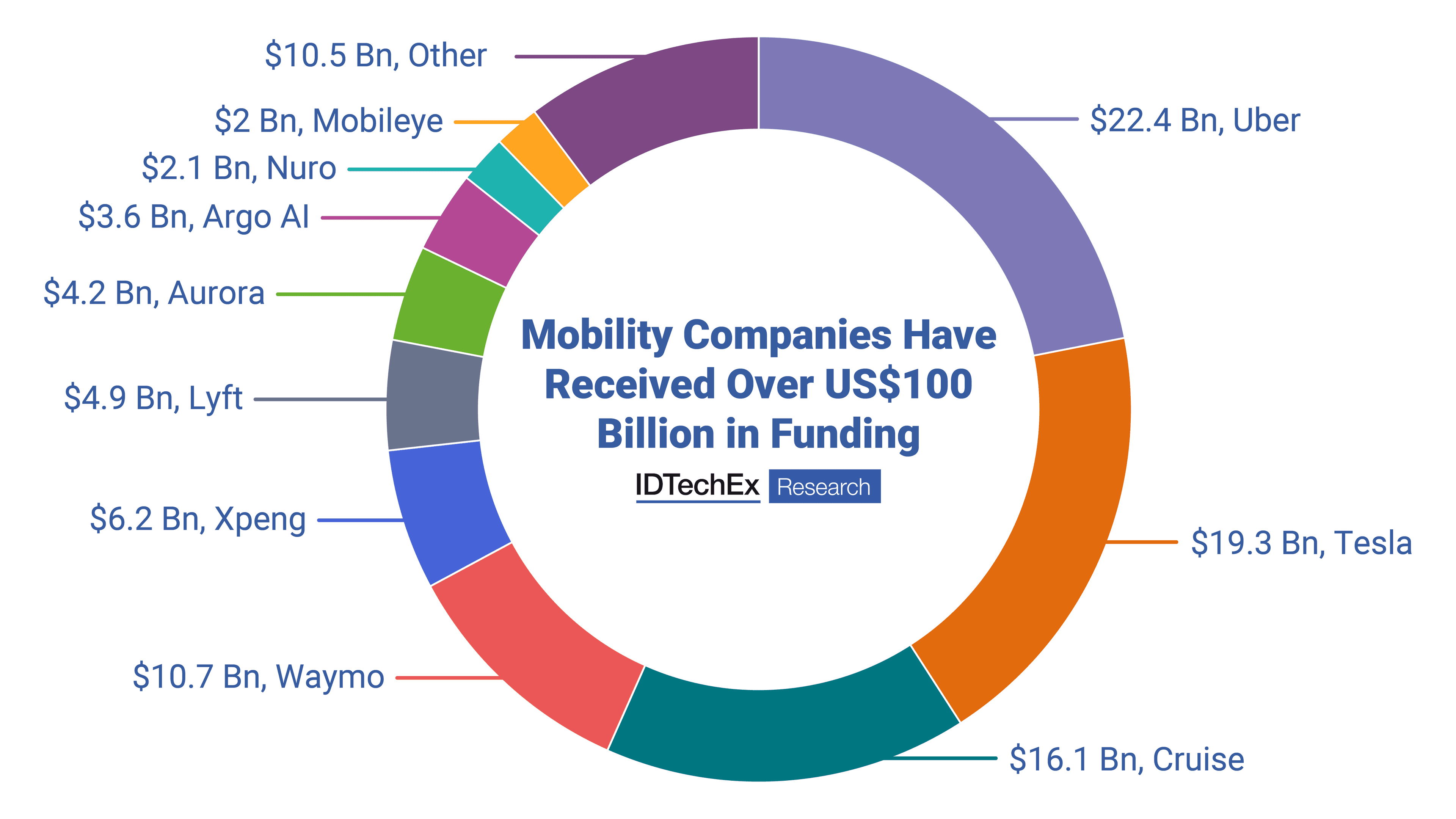

The pursuit of self-driving technology has been one of the most expensive engineering races in history. Industry and venture investors poured over 100 billion dollars into AV startups and programs over the past decade.

Some of this capital has not paid off: Argo AI’s shutdown in 2022 meant Ford and VW wrote off over $3.6B in investments, and Uber’s sale of its AV unit (ATG) to Aurora in 2021 reflected a retreat to focus on core business. The stock market also punished pure-play AV companies; for instance, by 2025 many SPAC-launched AV firms trade far below initial valuations.

That said, money is still flowing into targeted areas – notably autonomous trucking (which has clearer near-term revenue potential) and enabling technologies like sensors and AI chips. In 2023–24, we saw large deals such as Wayve (UK) securing $1B for AI-driven self-driving tech, and ongoing strategic investments by automakers in AI software companies. Tech giants (Alphabet, Amazon, Intel through Mobileye) continue to bankroll AV research, seeing it as a long-term strategic play.

The Road Ahead: Challenges and Opportunities

Regulatory and Safety Landscape

The regulatory and safety landscape remains a significant hurdle, as policymakers continue playing catch-up with rapid technological advances, creating fragmented and often inconsistent guidelines across regions. In the U.S., states like Arizona and Texas actively encourage autonomous deployments, while California has imposed stringent oversight after high-profile incidents involving companies like Cruise.

Europe’s regulatory environment is more cautious, permitting only limited Level 3 deployments under specific conditions, whereas China has aggressively supported autonomy through targeted policies in multiple cities.

Safety remains paramount—each autonomous mile logged without incident bolsters public trust, yet accidents like Cruise’s pedestrian collision in San Francisco underscore persistent vulnerabilities. As AV technology evolves toward fully driverless operation, regulators face critical decisions on liability, certification standards, and oversight mechanisms. Transparency around safety performance, coupled with consistent global regulatory frameworks, will be vital to broader acceptance and deployment. Ultimately, navigating these complex regulatory dynamics and reinforcing a robust safety track record are essential to unlocking autonomy’s transformative potential.

Closing the Gap to Level 5

The final vision – cars that can drive anywhere, in any conditions, without human input – remains the “north star” for the industry. 2025’s reality suggests it is still many years away. The last 1% of driving scenarios (think unanticipated construction detours, heavy snow-covered roads with obscured lane lines, or a person in a costume directing traffic) are incredibly hard for AI to handle. Companies will spend at least the rest of the decade chipping away at these corner cases. Advances in AI (for example, future neural network architectures or better simulation training using generative techniques) are expected to incrementally improve the vehicle’s ability to handle complexity. Some experts believe quantum computing or neuromorphic chips could eventually provide the leap needed for true Level 5. In the meantime, the likely path is gradual expansion: more cities for robotaxis, higher speed or more roads for hands-free driving in personal cars, and broader trucking routes for freight. Each success will come with new challenges – and each will inform the next.

Collaboration and Consolidation

The journey ahead will also be shaped by partnerships. We’ve seen that one company shouldering all aspects (software, hardware, fleet operations, etc.) is tough. Going forward, expect more collaborations like Toyota partnering with Pony.ai or multiple automakers aligning on common standards. Big tech and auto firms might form joint ventures to share costs and expertise. There may also be further consolidation: weaker players or those who achieved partial success may be acquired by stronger ones (similar to how Amazon bought Zoox). This means the competitive landscape in a few years could thin out to a handful of major platforms powering most autonomous vehicles, much like how a few aircraft manufacturers dominate aviation. Such consolidation could accelerate progress (by pooling talent and IP) or, conversely, slow innovation if competition diminishes – a balance regulators will watch.

Infrastructure and Integration

Achieving the full potential of AVs will require more than just the vehicles themselves. Infrastructure upgrades can greatly assist autonomy: for instance, V2X (vehicle-to-everything) communication systems where traffic lights broadcast their status to cars, or dedicated AV lanes on highways. Some cities are now investing in smart traffic management with the expectation of autonomous traffic. Urban planning might evolve to include AV pickup zones, robotic charging stations, and revised parking needs (a world with robotaxis needs fewer parking lots). Furthermore, autonomous cars will need to coexist with human drivers for a long time – hybrid traffic management will be crucial. Policymakers and industry groups are starting to develop standards for how AVs signal intentions to pedestrians (e.g. external displays or sounds) and how they should behave around emergency vehicles, school zones, etc. These integrations between technology and the physical world will be an ongoing effort and an opportunity for innovation.

Conclusion / Outlook

In summary, autonomous driving in 2025 is no longer science fiction – it’s an emerging reality with data-backed achievements and also a sobering appreciation of the remaining hurdles. The coming years will likely see more commercial deployments in constrained domains (from robo-taxis in select cities to autonomous semi-trucks on key freight corridors), bringing in the first real revenues for this industry.

Each incremental step builds the foundation of experience and public confidence needed to eventually broaden the scope. While the timeline to ubiquitous self-driving cars has stretched further out, the industry’s fact-based progress – millions of miles driven autonomously, improved safety statistics, and steadily growing market investment – provides a solid bedrock for optimism.

The consensus among developers is that autonomy will come in waves, not one big bang: we will wake up one day and realize our commute is handled by the car itself, not because of a sudden overnight breakthrough, but due to years of steady, behind-the-scenes advancement.

For investors, technologists, and the public, the task now is to navigate this marathon with patience, supporting innovations that bring us closer to safer, more efficient roads. The autonomous driving journey continues – with 2025 marking the end of the beginning, and the road ahead full of both challenges to solve and opportunities to seize.